Achieving financial stability and growth often feels like navigating a complex maze, especially in your 20s. Reflecting on my own journey, I realise there are key financial habits I wish I had embraced earlier.

This article delves into five essential financial habits that can significantly boost your income through hard work and dedication. Whether you’re just starting your career or looking to refine your financial strategy, these insights blend personal experiences with actionable advice to help you pave the way to financial success.

Introduction

Like many in my 20s, I embarked on my financial journey with enthusiasm but lacked a clear roadmap. Early career excitement often overshadows the importance of foundational financial habits. Over time, I learned that disciplined financial practices are crucial for long-term prosperity.

Why These Habits Matter

Financial habits formed in your 20s can set the stage for future wealth. According to a 2023 study by Bankrate, individuals who establish strong financial habits early are 30% more likely to achieve financial independence by age 40. These habits not only increase income but also ensure financial resilience against unexpected setbacks.

Common Financial Misconceptions in Early Career

Many young professionals believe that saving a small portion of their income or occasionally investing is sufficient. However, without a structured approach, these efforts often fall short. Misconceptions such as “I can start saving later” or “Investing is too complicated” can hinder financial growth.

What to Expect from the Article

In this article, we’ll explore five financial habits that can transform your income trajectory. Each habit is broken down with personal insights, practical examples, and real-world case studies to ensure you can implement them effectively.

Habit #1: Budget Automation That Actually Works 📱

Why Traditional Budgeting Often Fails

Traditional budgeting methods, like manually tracking expenses in spreadsheets, are time-consuming and prone to errors. They often lead to inconsistency, making it difficult to stick to financial goals.

Modern Tools vs. Spreadsheets

Modern budgeting tools such as Mint, YNAB (You Need A Budget), and Personal Capital automate expense tracking, categorize spending, and provide real-time insights. These tools eliminate the manual burden and enhance accuracy, making budgeting more manageable and effective.

Setting Realistic Spending Categories

Creating realistic spending categories is crucial. Overly restrictive budgets can lead to frustration, while vague categories fail to provide clear guidance. Aim for balanced categories that reflect your lifestyle and financial goals.

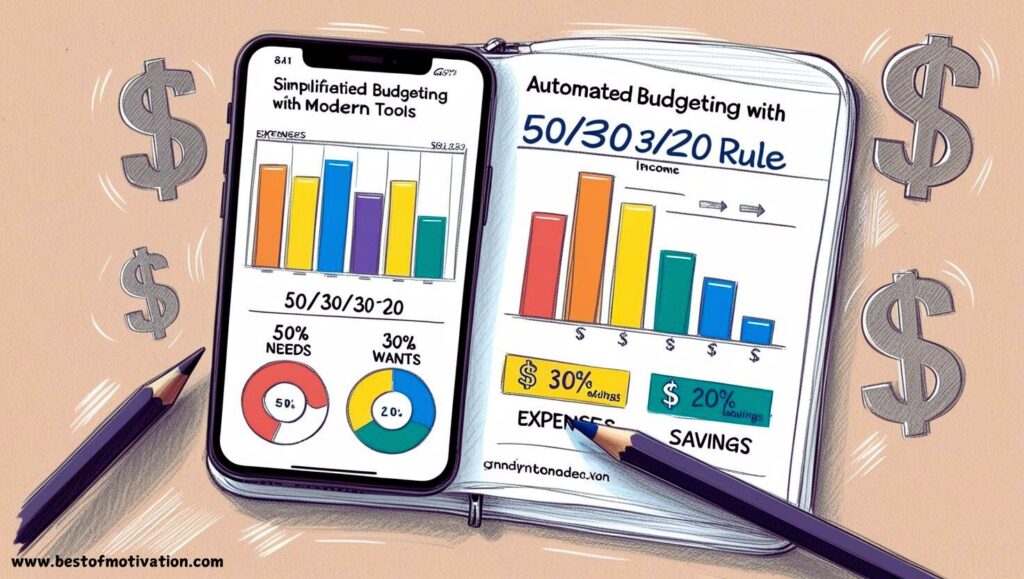

Practical Example: The 50/30/20 Rule in Action

The 50/30/20 rule divides your after-tax income into:

- 50% Needs: Rent, utilities, groceries.

- 30% Wants: Dining out, entertainment.

- 20% Savings and Debt Repayment: Emergency fund, investments, loan payments.

Using a budgeting app, you can set these allocations and receive alerts when you approach your limits, ensuring disciplined spending without feeling deprived.

Real Case Study: Before/After Automation

Before Automation: Sarah, a 25-year-old marketing professional, struggled with inconsistent savings and overspending on non-essentials. She manually tracked expenses, leading to missed savings goals.

After Automation: By switching to YNAB, Sarah automated her budget, categorized expenses, and set clear financial goals. Within six months, she increased her savings rate by 25% and paid off $5,000 in credit card debt.

Habit #2: Emergency Fund Strategy for Real Life 🛡️

Moving Beyond the “6 Months” Rule

While the “6 months of expenses” rule is a good benchmark, it may not be realistic for everyone. Factors like job stability, industry volatility, and personal responsibilities should influence the size of your emergency fund.

How to Build It Without Sacrificing Quality of Life

Start by setting smaller, achievable goals. Aim for a $1,000 starter emergency fund, then gradually build up to cover 3-6 months of expenses. Automate transfers to your emergency fund account to ensure consistent contributions without impacting your daily budget.

Where to Keep Emergency Money (and Why)

Store your emergency fund in a high-yield savings account or a money market account. These options offer liquidity and modest interest, ensuring your money is accessible when needed while earning some returns.

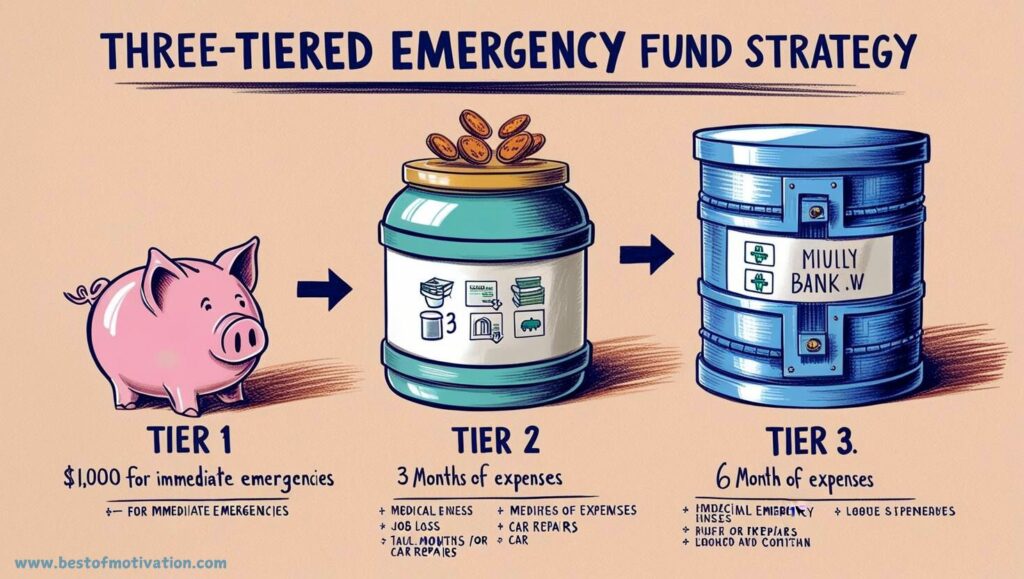

Practical Example: Tiered Emergency Funding

Implement a tiered approach:

- Tier 1: $1,000 for immediate emergencies.

- Tier 2: 3 months of expenses for larger unexpected costs.

- Tier 3: 6 months of expenses for major life changes (e.g., job loss, medical emergencies).

This strategy allows flexibility and prioritizes urgent needs first.

Common Emergencies and How to Prepare

Typical emergencies include medical expenses, car repairs, or job loss. By understanding potential risks and planning accordingly, you can mitigate financial stress and maintain stability during challenging times.

Habit #3: Investment Fundamentals Without the Jargon 📈

Understanding Risk Tolerance Realistically

Assessing your risk tolerance involves evaluating your comfort with market fluctuations and potential losses. Tools like Vanguard’s Risk Tolerance Questionnaire can help determine the right investment strategy for your personality and financial goals.

Index Funds vs. Individual Stocks

Index Funds offer diversified exposure to the market with lower risk and fees, making them ideal for beginners. Individual Stocks can yield higher returns but come with increased volatility and the need for extensive research.

How to Start with Limited Funds

Start investing with platforms like Robinhood, Acorns, or Stash, which allow you to invest small amounts. Utilize Robo-advisors like Betterment or Wealthfront to automate and optimize your investment portfolio based on your risk tolerance and goals.

Practical Example: Building a Basic Portfolio

Allocate your investments as follows:

- 60% Index Funds: Provides broad market exposure.

- 20% Bonds: Adds stability and reduces risk.

- 20% Individual Stocks or ETFs: Offers growth potential.

This balanced approach ensures diversification and mitigates risk while aiming for steady growth.

Common Investment Mistakes to Avoid

Avoid timing the market, over-diversifying, and neglecting fees. Consistently invest, focus on long-term growth, and be mindful of costs to maximize your investment returns.

Habit #4: Debt Management & Credit Building 💳

Strategic Debt Handling

Prioritize high-interest debts first using the debt avalanche method or focus on smaller debts with the debt snowballmethod to build momentum. Consolidate debts where possible to reduce interest rates and simplify payments.

Credit Score Optimization

Maintain a good credit score by:

- Paying bills on time.

- Keeping credit utilization below 30%.

- Avoiding unnecessary credit inquiries.

- Regularly checking your credit report for errors.

A strong credit score can lead to better loan terms, lower interest rates, and increased financial opportunities.

When to Use Credit vs. Debit

Use credit for purchases that can be paid off monthly to build credit history and earn rewards. Use debit for everyday expenses to avoid overspending and accumulating debt.

Practical Example: Debt Snowball Method

Start by listing all debts from smallest to largest:

- Pay minimum payments on all debts except the smallest.

- Allocate extra funds to the smallest debt until it’s paid off.

- Move to the next smallest debt, repeating the process.

This method builds momentum and provides psychological wins as each debt is eliminated.

Tools for Tracking and Improvement

Utilize tools like Credit Karma, Mint, or Debt Payoff Planner to monitor your credit score, track debt repayment progress, and receive personalized recommendations for improvement.

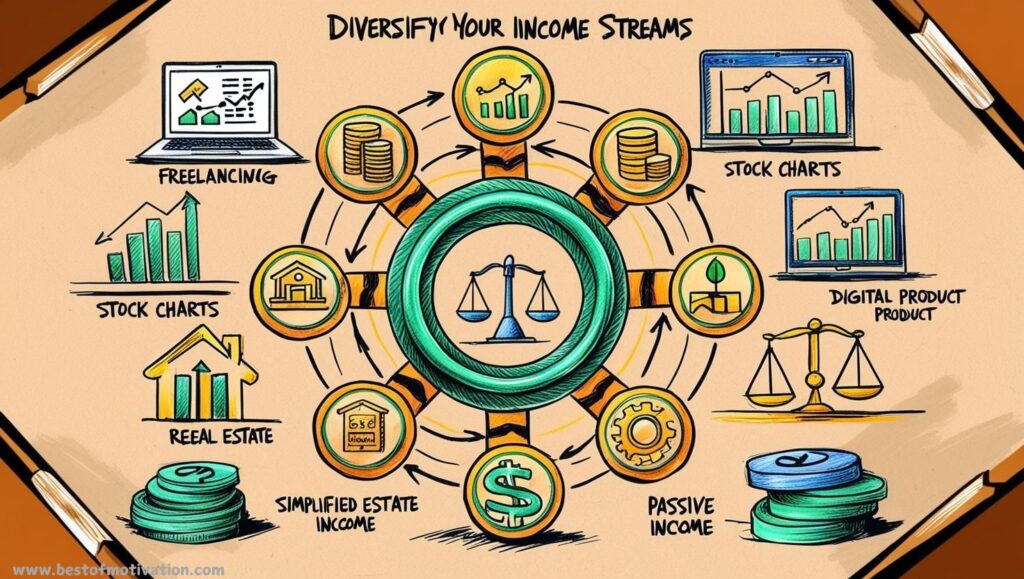

Habit #5: Income Diversification Strategies 💰

Beyond the Side Hustle Hype

While side hustles are popular, true income diversification involves multiple streams that vary in effort and risk. This can include investments, passive income sources, and leveraging existing skills.

Evaluating Additional Income Sources

Assess potential income streams based on your skills, interests, and available time. Consider options like freelance work, rental income, dividend investing, or creating digital products.

Advertisement

Upgrade Your Skills Online

Professional certificates from \$19

Time vs. Money Trade-Offs

Understand the balance between time and money. Some income streams require significant upfront time investment but offer passive returns later, such as writing an e-book or developing an online course.

Practical Example: Skill Monetization

If you’re proficient in graphic design, consider offering freelance services on platforms like Upwork or Fiverr. Alternatively, create and sell design templates on Etsy or Creative Market to generate passive income.

Risk Assessment of Different Income Streams

Evaluate the risks associated with each income stream, including market volatility, initial investment, and time commitment. Diversify across low-risk and high-risk opportunities to balance potential rewards with stability.

📌 Pin it to your Pinterest board and share these essential tips with your friends and family to inspire financial growth and stability!

Real-World Implementation

Monthly Action Checklist

- Automate Budgeting: Set up a budgeting app and automate transfers.

- Build Emergency Fund: Allocate a fixed percentage of income monthly.

- Start Investing: Open an investment account and make your first investment.

- Manage Debt: Implement a debt repayment strategy.

- Explore Income Streams: Identify and start developing additional income sources.

Progress Tracking Methods

Use financial tracking tools and apps to monitor your progress. Regularly review your budget, investment portfolio, debt repayment, and income streams to ensure alignment with your goals.

Adjusting for Different Income Levels

Tailor your financial habits based on your income. Higher earners can allocate more towards investments and savings, while those with lower incomes should prioritize essential expenses and gradual debt reduction.

Common Obstacles and Solutions

- Lack of Time: Automate as much as possible and set aside specific times for financial tasks.

- Unexpected Expenses: Maintain a robust emergency fund to cushion against surprises.

- Motivation Drops: Set short-term milestones and celebrate small victories to stay motivated.

Conclusion

Long-Term Impact of These Habits

Adopting these five financial habits can transform your financial landscape, leading to increased income, reduced debt, and long-term wealth. Consistent application fosters financial resilience and opens doors to opportunities you might not have imagined.

Key Takeaways

- Automate Your Budget: Simplify financial management with modern tools.

- Build a Realistic Emergency Fund: Prepare for life’s unpredictability without sacrificing quality of life.

- Invest Wisely: Start early, diversify, and avoid common pitfalls.

- Manage Debt Strategically: Optimize your credit and handle debts efficiently.

- Diversify Income Streams: Expand your earning potential through multiple avenues.

Next Steps for Readers

Begin by implementing one habit at a time. Assess your current financial situation, set clear goals, and utilize the tools and strategies discussed to enhance your financial health. Remember, consistency and dedication are key to achieving financial success.

Additional Resources

Recommended Apps and Tools

- Budgeting: YNAB, Mint

- Investing: Robinhood, Betterment

- Debt Management: Debt Payoff Planner, Credit Karma

Further Reading

- “The Total Money Makeover” by Dave Ramsey

- “Rich Dad Poor Dad” by Robert Kiyosaki

- “Your Money or Your Life” by Vicki Robin

Free Calculators

Ready to make smarter financial decisions? Use our free calculators for savings, investments, budgeting, and debt management. Head over to bestofmotivation.com/financial-calculators and take the first step towards financial success!

Community Resources

- Reddit: r/personalfinance

- Facebook Groups: Personal Finance for Young Adults

- Local Workshops: Check community centers or financial institutions for free seminars.

By integrating these financial habits into your daily routine, you set yourself up for a future of financial freedom and security. Embrace the journey with dedication and watch your income grow through consistent, informed actions.